As legislators indicated, in connection with the introduction of a fee to compensate for damage caused by heavy vehicles to public roads of federal significance, the financial burden on the owners of such vehicles has increased significantly. After all, these persons must pay two mandatory payments to the consolidated budget of the Russian Federation for the financing of public roads: a fee for compensation of damage and a transport tax. They decided to correct this “injustice” (though not for long). Let's find out how.

The answer is contained in Federal Law No. 249-FZ dated July 3, 2016, which amended Part II of the Tax Code of the Russian Federation. This law came into force on July 3, 2016, but the effect of the articles of the Tax Code of the Russian Federation amended by it is determined in a special manner. Let's start with the order in which organizations that own heavy vehicles must now calculate transport tax.

Tax deduction for transport tax from an organization

If a transport company, to which a vehicle is registered, having a permissible maximum weight of over 12 tons and included in the register of vehicles of the toll collection system (the so-called “Platon” system), pays a fee to compensate for the damage caused to federal roads by the specified vehicle, it has the opportunity reduce your transport tax liability.

The relevant provisions on this are included in paragraph 2 of Art. 362 of the Tax Code of the Russian Federation (new additional paragraphs 12 – 14). The basic rule goes like this.

The amount of tax calculated at the end of the tax period by taxpayer organizations in relation to each vehicle with a maximum permitted weight of over 12 tons registered in the register is reduced by the amount of the fee paid in respect of such a vehicle in a given tax period.

Thus, reducing the financial burden on organizations that own heavy vehicles is realized through the use of tax deductions.

It must be taken into account that the amount of the fee transferred during the tax period (that is, the calendar year) for a specific heavy-duty vehicle reduces the amount of the transport tax calculated based on the results of the specified period for this particular vehicle.

It is possible that the amount of the fee paid exceeds the amount of transport tax calculated at the end of the year. When applying a tax deduction, this essentially means that the amount of tax payable to the budget takes on a negative value. So, in this case, the amount of transport tax should be considered equal to zero (paragraph 13, paragraph 2, article 362 of the Tax Code of the Russian Federation).

You should also pay attention to the new paragraph (paragraph 2) in paragraph 2 of Art. 363 Tax Code of the Russian Federation.

Taxpayers-organizations do not pay calculated advance tax payments in relation to a vehicle with a permissible maximum weight of over 12 tons, registered in the register.

Let us remind you that, as a general rule, during the tax period, taxpayers-organizations must pay advance payments for transport tax, unless otherwise provided by the laws of the constituent entities of the Russian Federation. Taking into account the innovation, advance payments in any case (regardless of what is determined by the law of the subject of the Russian Federation) do not need to be paid for heavy vehicles included in the vehicle register of the toll collection system (but they need to be calculated, why, it will become clear later). For other taxable vehicles, advance payments are calculated and transferred, except for situations where otherwise established by the law of a constituent entity of the Russian Federation.

Reducing transport tax

From July 3, 2021, transport tax can be reduced for payments to the Platon system . The payment reduces the amount of transport tax only for a specific truck weighing over 12 tons.

A company can take into account only one of two possible amounts as expenses:

- transport tax, which was reduced by the road tax if the tax was less than the tax;

- portion of the toll that exceeds the tax.

If a company has overpaid advances on transport tax for a cargo vehicle, they can be returned at the end of the year.

The question often arises: do you need to pay transport tax if you pay Platon?

If the amount payable to the system is equal to or greater than the amount of transport tax, you do not need to pay tax. If the fee is less, the owner reduces the tax by the amount he paid.

How to reduce transport tax on Platon?

Procedure for applying for tax reduction benefits, documents

Legal entities and individuals are in an equal position when it comes to the calculation and payment of transport tax. The tax is paid based on a notification from the Federal Tax Service.

To apply the benefit, the Federal Tax Service provides the following documents:

- statement;

- information about the owner of the vehicle (documents confirming ownership);

- vehicle passport (indicating the permitted weight over 12 tons);

- information on making payments for using the trails.

It is recommended to use extracts from the system’s Personal Account.

Documents are provided in person, through a representative, sent by mail (along with a list of attachments), through the Public Servants Portal (https://www.gosuslugi.ru/10054) or the “Taxpayer Personal Account” service (https://lkfl.nalog .ru/lk/).

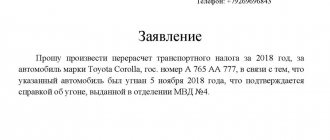

An application for the “Platonov” benefit is sent to the Federal Tax Service before the tax inspectorate begins to generate notifications for the expired tax period.

The application is drawn up in two copies . The first is given to the inspection, the second remains with the applicant. Request that the inspector affix a stamp indicating acceptance of the application and documents from the current date.

The amount of transport tax, which is subject to transfer to the budget by car owners, is calculated by the tax authorities. Grounds - information provided to tax authorities by the authorities carrying out state registration of vehicles.

If the taxpayer is late in submitting the application, he remains entitled to the benefit. The amount of overpaid tax due to recalculation is returned for the period of recalculation.

An application for the return of overpaid funds must be submitted within three years from the date of payment of this amount. This means that individuals can provide documents that confirm their right to a deduction under the Platon system within three years from the date the right to the benefit arises.

Let’s find out how to include “Plato” in transport tax:

- At the end of the year, pay the difference between the tax and the fee for the year. The amount is taken from the operator's report. If the fee is greater than the tax, it may not be paid.

- In line 280 of the Tax Declaration, enter the code 40200. In line 290 - the fee for the year. Line 300 is the tax that was reduced by the fee. If the fee is larger, enter 0.

- In tax accounting, the difference between “Plato” and tax is taken into account in expenses. Example: the tax for the year was 14,000 rubles, the fee to the system was 11,000 rubles. Take into account only 3,000 rubles of tax.

- Advance tax payments on heavy goods vehicles can be calculated, but do not have to be paid. They are not reflected in the declaration. Calculated advance payments are also not taken into account in expenses.

The declaration is easy to fill out, but you must first confirm payment of the fee for using federal highways. Without this, the deduction will not apply.

Let's find out how to confirm the transport tax benefit using the Platon system.

Confirmation procedure

Car owners have the right to confirm the deduction if they meet the following conditions:

- vehicle weight exceeds 12 tons;

- The vehicle is included in a special register;

- the system submitted a report on the payment.

The report is generated once a year . It can be ordered through the official website or mobile application. First, create an account and enter the required information about the vehicle.

If it is more convenient for you to receive documents in paper form rather than electronically, go to the Platon representative office.

They also use their personal account:

- They go to the vehicles section, find the desired car, which gives the right to a deduction.

- In the “Request a Federal Tax Service certificate” section, indicate the period and confirm the entered data.

- The document will be automatically downloaded.

- The file is protected by an electronic signature. It is served without printing.

This document and other information about the vehicle owner will help you obtain a tax break. If you own several heavy trucks, repeat the above steps for each of them.

When is it impossible to reduce transport tax?

If the payers of the transport tax and the system are different persons, the deduction does not apply . This procedure is valid if the car is leased.

The heavy truck is registered to the lessor, but the recipient of the service (the one who moves the cargo on the vehicle) pays for the use of the routes.

Payment amounts are made not by the owner, but by the lessee . This solution to the problem is very fair, since the costs are borne by different individuals or companies.

The state system “Platon” was created to attract extra-budgetary funds for the development of road infrastructure. All funds received are used for road repair and development.

More than 25 billion rubles have already been collected for the Road Fund (https://www.rtits.ru/ru/press_centr/press_relizi/1/102).

There are more than 50,000 federal roads in the system. You can reduce transport tax using the Platon system . You only need to confirm your right to the benefit and also submit the necessary documents to the tax office.

Video: Plato reduces transport tax

Transport tax benefit for individuals

Individuals (including those registered as individual entrepreneurs) on the basis of the new Art.

361.1 of the Tax Code of the Russian Federation are exempt from transport tax in relation to a heavy vehicle if the amount of the “Platonovsky” fee transferred during the tax period exceeds or equals the amount of the calculated tax for this period. If the amount of the calculated transport tax exceeds the amount of the fee, a tax benefit is provided in the amount of the fee. Accordingly, the difference is paid to the budget. In order to take advantage of the announced tax benefit, an individual must submit to the tax authority:

- application for benefits;

- documents confirming the right to receive it.

It should be taken into account that the use of benefits in relation to heavy vehicles is the right (not the obligation) of an individual – a transport tax payer. Therefore, if the choice made is not declared (by submitting the relevant documents to the tax authority), the exemption will not apply. Let us recall that the calculation of the amount of transport tax to be transferred to the budget by individual taxpayers is carried out by the tax authority on the basis of information provided by the authorities carrying out state registration of vehicles (clause 1 of Article 362 of the Tax Code of the Russian Federation).

Accounting for fees when calculating corporate income tax

The amount of the “Platonovsky” fee used as a tax deduction for transport tax is not taken into account when calculating profit tax by the transport company.

On this score in Art. 270 of the Tax Code of the Russian Federation now has a special norm - clause 48.21. Based on the results of reporting periods, the amount of payment not taken into account when determining the tax base for income tax is determined based on the amount of advance payments calculated in accordance with Chapter. 28 of the Tax Code of the Russian Federation in relation to heavy vehicles. But the difference (if the amount of the transferred fee exceeds the amount of the transport tax) is included in tax expenses on the basis of paragraphs. 49 clause 1 art. 264 of the Tax Code of the Russian Federation (other expenses associated with production and sales). (Subparagraph 1 does not work, since, as financiers indicated in Letter No. 03-05-06-04/77196 dated December 29, 2015, payment for compensation for damage caused to public roads of federal significance by heavy vehicles does not apply to taxes and fees regulated by the Tax Code.) Serve as supporting documents in relation to expenses in the form of “Platonic” fees (letters of the Ministry of Finance of the Russian Federation dated January 11, 2016 No. 03-03-RZ/64, dated December 28, 2015 No. 03-03-06/1 /76740):

- operator’s report, which indicates the route of the vehicle with reference to the time (date) of the start and end of the vehicle’s movement;

- primary accounting documents drawn up by the taxpayer himself, justifying the use of the named vehicle on the corresponding route.

Reflection of the “Platonov” fee in the transport tax return

The transport tax declaration, in which the taxpayer can indicate a tax benefit and (or) deduction for a vehicle with a permissible maximum weight of over 12 tons, was approved by Order of the Federal Tax Service of the Russian Federation dated December 5, 2016 No. ММВ-7-21/ [email protected]

Despite the fact that the Order of the Federal Tax Service is in effect starting with the submission of a tax return for 2021, those taxpayers who need to apply the heavy-duty exemption could already report using the new form for 2021 (clause 3 of the Letter of the Federal Tax Service of the Russian Federation dated December 29, 2016. No. PA-4-21/ [email protected] ).

Payment as an expense for the “simplified”

If a transport company (IP) applies the simplified tax system with income selected as the object of taxation, reduced by the amount of expenses, it has the opportunity to act in accordance with a procedure similar to that established for income tax payers.

To be more precise: in tax expenses, “simplified” workers can include the amount of excess of the payment paid during the tax period for damages over the amount of transport tax calculated for the tax period (new paragraph 37 in paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation). When calculating advance payments for tax paid in connection with the application of the simplified tax system, expenses take into account the amount of the “Platonov” fee actually paid for the reporting period, reduced by the amount of calculated advance payments for transport tax. The same applies to Unified Agricultural Tax payers - a new clause talks about this. 45 in paragraph 2 of Art. 346.5 Tax Code of the Russian Federation.

For your information

Previously, “simplified” people were deprived of the opportunity to include the “Platonov” fee in tax expenses (letters of the Ministry of Finance of the Russian Federation dated January 18, 2016 No. 031106/2/1319, dated October 6, 2015 No. 03‑11‑11/57133).

Validity period of innovations

The possibility of applying tax deductions for transport tax by organizations applies to legal relations that arose from 01/01/2016, and is valid until 12/31/2018 inclusive.

During the same period, accordingly, tax expenses (when applying a regular or simplified taxation system) are formed taking into account the amount of the “Platonic” fee offset against the transport tax reduction (it is not taken into account as expenses). From 01/01/2019, tax deductions will no longer be applicable, but the possibility of including the amount of compensation for damages in tax expenses will remain. Individuals can use the tax benefit (exemption from taxation) for transport tax in relation to legal relations that arose starting from 01/01/2015. The benefit will cease to apply from 01/01/2019.

It should be especially emphasized that a tax deduction (benefit) for transport tax is provided to taxpayers of transport tax in connection with their payment of compensation for damage in respect of vehicles with a maximum permitted weight of over 12 tons. Therefore, if, for example, in relation to heavy vehicles registered to the lessor, the “Platonic” fee is paid by the lessee, then the lessor has no right to reduce the transport tax by the amount of the fee paid by the lessee to compensate for damage (Letter of the Ministry of Finance of the Russian Federation dated July 18, 2016 No. 03‑ 05‑04‑04/41940).

Registration of a car in the traffic police and the Platon system

All vehicles (TS) are subject to mandatory state registration (clause 1 of Article 358 of the Tax Code of the Russian Federation, Order of the Ministry of Internal Affairs of the Russian Federation dated November 24, 2008 N 1001).

Vehicles with a permissible maximum weight of over 12 tons, if their route passes along federal highways, must be registered in the Platon system (Article 31.1 of the Federal Law of November 8, 2007 N 257-FZ).

Registration of a vehicle with the State Traffic Safety Inspectorate, as well as registration in the Platon system, is completed in the information register Registration of vehicles - type of operation Registration in the section Directories - Taxes - Transport tax - Registration of vehicles.

Vehicle Registration form indicates:

- Fixed asset - a registered vehicle is selected from the Fixed Assets directory .

- Date – date of registration with the State Traffic Safety Inspectorate and (or) date of registration in the Platon system.

- Tax rate is set automatically by the program.

- check the box Registered in the register of the Platon system : The Scania P360 flatbed tractor is a truck for which the fee is paid to Platon.