In the insurance market, the Russian Union of Auto Insurers has been regulating relationships between MTPL participants for more than ten years, protecting the interests of clients of insurance companies that have ceased their activities due to bankruptcy.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

+7 (499) 938-81-90 (Moscow)

+7 (812) 467-32-77 (Saint Petersburg)

8 (800) 301-79-36 (Regions)

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

He develops and implements into practice the insurance market a methodology for improving insurance mechanisms for compulsory motor liability insurance.

Along with the creation of its database, a new era has opened in the insurance market, which must be carried out without fail by vehicle owners.

The leading role in the activities of the RCA is given to the application of standards and regulations in services for compulsory motor third party liability insurance and the development of statistics.

What it is

The Russian Union of Auto Insurers is a non-profit organization. Its status is approved by current legislation, therefore it became the first unified all-Russian professional association in the insurance services market, which is carried out by compulsory motor liability insurance. Its formation was based on the principle of compulsory membership of insurers.

The primary goal of the RCA is to ensure interaction between vehicle owners and draw up rules of professional activity for the production of compulsory insurance.

The Union was founded in August 2002 on the initiative of the most prominent insurance companies of the Federation, which was registered in October of the same year in the unified register of insurers and associations of the Ministry of the Russian Federation.

The activities of the RCA are carried out in accordance with the instructions of the Federal Law “On Compulsory Insurance of Civil Liability of Vehicle Owners”. It was adopted in April 2002 as number 40.

Insurance companies are current members and observers of the RSA

Currently, 70 companies are members of the RCA. Among them we can note such well-known ones as Ingosstrakh and Rosgosstrakh.

9 insurance agencies are members of the RSA as observers. Below is a list of these associations:

- "Avangard-Garand";

- "Granta"

- "Intouch Insurance";

- "KSA-Kluwer";

- “National Insurance Traditions”;

- "RSHB-Insurance";

- "Insurance investments";

- "SK TIT";

- "CSO".

With the exception of KSA-Kluver, registered in Kazan, from Crimea, and the Insurance Investments company from Ufa, all other RSA observers are registered in Moscow or the Moscow region.

Currently, the RSA register lists 19 insurance companies whose licenses have been terminated.

In this case, we are talking about the voluntary withdrawal of an organization from the union. In other cases, companies were reorganized and merged with larger organizations.

As of July 2021, the Moscow company and the auto insurer “Insurance Support” from the city of Ryazan had their licenses for insurance activities frozen. The license of the Moscow insurer BIN-Strakhovanie is currently limited.

What functions does it perform?

RSA compensates for losses incurred under compulsory motor liability insurance in accordance with accepted obligations in accordance with regulations. The procedure for making payments is approved by current legislation.

Compensation for injuries caused to life and health is made in the following situations, when the culprit of the road traffic accident occurs:

- was not installed;

- he did not have a compulsory motor liability insurance agreement.

Payments for compensation for damage caused to the property of citizens of the Federation are made:

- if the insurance company goes bankrupt;

- her license under which she carried out economic activities was revoked.

To receive compensation, the policyholder must submit to the RSA a package of documents that contains:

- application requesting payment of compensation;

- documents on the insured event certifying the accident;

- notification that an accident has occurred;

- a certificate of an accident issued by the traffic police on a unified form numbered 12, 31, 11 or 748;

- a copy of the protocol recording an administrative offense issued as a result of an accident or a decision of the traffic police on the application of an administrative measure;

- a copy of the resolution on the case opened in connection with an administrative offense;

- the original of the MTPL insurance policy concluded by the culprit of the accident with the insurance company;

- if there was a trial, then the original of the court decision on sanctions;

- act of independent technical examination of the condition of the vehicle.

RSA considers the application within 30 calendar days, counted from the date of its registration in the journal of incoming correspondence.

But if additional materials on the case are required, the duration of the consideration increases. He makes payments by bank transfer.

If your claim for payment of compensation is refused, you must file a claim in court.

SAR functions

The professional association of insurers in the insurance market performs a number of important functions:

- streamlines the process of interactions between members of the union;

- develops and implements insurance rules mandatory for all members, and subsequently assumes the functions of monitoring their implementation;

- carries out representative functions in government bodies;

- provides compensation payments to victims of road accidents.

In RSA, the most important thing is the reserve fund, from which compensation payments are made. This fund is formed from contributions from RSA members and amounts to at least 3% of collected insurance premiums.

PCA is beneficial for all participants in the insurance process:

- To insurance companies:

- protection and assistance in the insurance process under compulsory motor liability insurance;

- supply of MTPL policy forms;

- assuming responsibility to the company's clients in the event of bankruptcy.

- For car owners:

- in some cases, when payment under standard compulsory motor liability insurance is not possible, compensation for damage caused in an accident;

- protection from unscrupulous insurance companies. For example, when imposing additional products, there is an unreasonable refusal to issue an MTPL policy.

Insurance rules

The information in the AIS database contains the official data of the owner, namely his full name, date of birth, including information about the series, driver's license number.

An insurance company, when concluding a compulsory motor liability insurance agreement with vehicle owners, is obliged to use AIS information about past concluded contracts in order to justify the bonus-malus coefficient that affects the cost of the policy.

It establishes 13 classes of insurance for vehicle owners for the application of coefficients commensurate with them. Until the beginning of 2013, the discount was assigned without written documents based on an oral application from the policyholder.

If during the last two years of insurance there were accidents committed by the policyholder, about which he did not notify the insurance company, then it has the right to refuse to make payment upon the occurrence of an insured event.

However, since 2013, rules have been adopted according to which the responsibilities of insurance companies are entrusted with conducting checks using a unified database of the bonus-malus coefficient in compulsory motor liability insurance.

Moreover, the activities of the insurance company over the previous 10 years and accident-free behavior over the past two years are checked. When calculating the cost of compulsory motor liability insurance, inspection data is used.

The association has created a database that makes it possible to calculate tariffs for compulsory motor insurance, taking into account the driver’s insurance history, and check the bonus-malus coefficients - AIS KBM.

The specified coefficient is used in calculating the insurance tariff and provides the opportunity to receive a bonus in the amount of 5% if the owner does not cause an accident on the road during the year.

If he committed an accident in the last two years, then the tariff increases, that is, the “malus” coefficient is accepted. If there is no information in the database about the use of the bonus-malus coefficient, a coefficient equal to one is used in the calculation.

If there is no information in the KBM AIS database, you must contact the insurance company where the previous OSAGO policy was concluded to enter the required data into the general database.

The unified MTPL database contains information about applicable discounts and increasing coefficients intended for owners of MTPL contracts.

Information is submitted to the unified database by local insurance companies operating in the Federation. In September 2014, a deadline was set for providing information to the AIS RSA on the conclusion of an MTPL agreement.

It must be provided within one working day after the day of its conclusion. Each specific situation is considered individually, so the amount of payments is calculated separately taking into account the prevailing circumstances.

However, the amount of compensation payments to the injured party for a specific road accident is strictly limited, so if several people were injured as a result of an accident, then the amount of compensation does not exceed 240 thousand , one - 160 thousand rubles .

OSAGO insurance rules.

When formulated as “damage to property”, the amount is:

| in the presence of several victims | no more than 160 thousand rubles |

| one victim | 120 thousand rubles |

Find out how to calculate the penalty for compulsory motor liability insurance in the article: penalty for compulsory motor liability insurance. Is life insurance compulsory for compulsory motor liability insurance? You can read here.

How to calculate bonus malus

Each traffic participant can easily independently determine the coefficient that is based on the new validity period of the compulsory motor liability insurance policy. All you need is a special table, which has been unchanged since 2003.

Upon first contact, each driver is assigned insurance class 3. At the end of the year, look at the table to see how many requests there were:

- no payments;

- from 1 to 4 or more payments.

Depending on the presence or absence of payment, the value of the coefficient for the new term is determined. To determine the indicator, you should look at the line with the current class for the coefficient for the new term.

For example, according to a previously issued compulsory motor liability insurance, the driver had a 6th accident class, which corresponds to a 15% discount. Since he was not the culprit of the accident during the year, when drawing up a new contract there will be a 7th class, which corresponds to a 20% discount.

If a driver with accident class 6 had 2 accidents during the year due to his fault, then under the new contract there will not be a discount, but an increasing indicator of 2, which corresponds to a coefficient of 1.4.

Legislation _

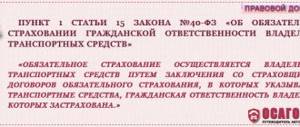

It is important to take into account that the KBM indicator was approved at the legislative level and reflected in 40 Federal Laws of April 5, 2002. According to Article 9 of the law, the base tariff for each vehicle and correction factors are determined, which depend on the insurance conditions.

Article 15 of the law defines the procedure for drawing up an agreement. Having studied it, it will become clear that the representative of the insurance company is obliged not only to request information in a single database, but also to provide information after issuing the OSAGO form.

For convenience, we offer it on our portal. After studying, you can ask your questions through the “Add a comment” form or to a consultant on our portal.

Calculation of the cost of compulsory motor liability insurance in RSA

The cost of an MTPL policy is formed from tariffs and coefficients. Insurance companies are unable to change its value. They do not have the right to assign discounts, make gifts, or hold promotions when purchasing a policy.

The state has established base rates, which are assigned depending on the type of car and coefficients that increase or decrease it depending on the conditions of previously completed insurance.

The coefficients express the main risks for the owners and the car they own:

- the driver's experience, his age;

- car registration area;

- car power;

- the number of persons who have the right to drive a car;

- driving without creating emergency situations.

There are no restrictions on driver age. But if the driver’s age is less than 22 years and his experience is less than three years, then he is assigned an increasing factor of 1.7, while for a more experienced driver its value will be equal to one.

Each district is assigned an individual territorial coefficient, for example, for Moscow, where the probability of an accident is high, a coefficient with a high indicator of 2 is assigned, for residents of the Moscow region it is equal to 1.7.

Engine power, expressed in horsepower, also affects the coefficient, which varies from 0.6 to 1.6;

If the car is driven by several people, then the coefficient is assumed to be 1.8; for a specific number of people driving the car, the coefficient will not exceed one.

The numerical value of the bonus-malus coefficient is directly dependent on the insured events that occurred previously, since it encourages driving without causing accidents.

Its minimum value is 0.5, and its maximum value is 2.4. To calculate the policy, a special formula is used, which includes the values of the tariff and coefficients.

Calculation example. Let's say we have a passenger car with a horsepower of 110, which is registered in the Moscow region.

It is driven by a driver who has reached 21 years of age and has a driving experience of two years. The number of persons allowed to drive is limited, the driving was carried out without accidents, insurance under compulsory motor liability insurance was concluded for the first time.

The following indicators are set:

| base rate | 1980 |

| coefficient reflecting age and experience | 1,7 |

| territorial coefficient | 1,7 |

| coefficient for limiting admitted persons | 1,0 |

| engine power factor | 1,2 |

| bonus-malus ratio | 1,0 |

The cost of a policy for a period of one year will be:

What is e-OSAGO?

An electronic policy is an analogue of a paper one with equal legal force (what does such a document look like?). The electronic version is completely virtual, since the document registration process is carried out remotely.

Paper certificates are filled out on GOZNAK form. After issuing an e-policy, the policyholder will receive a document in a pdf file by email. The information contained in it is reflected in the same way as on paper. The electronic MTPL must be printed in order to be presented to traffic police officers upon request.

Reference. The appearance of the e-certificate is practically no different from the paper one. It can be color or black and white. The background is simpler, since the microknot is applied only to a regular policy to protect against counterfeiting.

OSAGO E-certificates are characterized by a unique series (ХХХ) , which has no analogues among paper documents.

Check the policy for authenticity

In the last few years, cases of theft of MTPL policies have become more frequent, and counterfeits have been discovered. When purchasing it from an insurance agent, it is better to check that it belongs to a specific insurance company, so that unforeseen situations with unpleasant consequences do not arise later.

To check the authenticity of the policy, you must enter the number into the RSA database, where its stamp and name must match.

It will help establish registration of the policy in a single registry. If the result of the check is: “the policy is lost,” you need to refuse to purchase it in order to subsequently conclude an insurance contract, then notify the insurance company.

In addition to the above, it should be noted that the PSA acts in favor of the driver, helping to ensure his protection.

The measures it takes to resolve disputes and make insurance payments emphasize the importance of this organization.

Further development of the activities of the RSA, improvement of its mechanisms will make it possible to increase insurance payments and introduce price tables according to which compensation will be paid to persons injured in road accidents.

Features of the OSAGO policy in the company Soglasie, find in the article: OSAGO Soglasie. This article describes payments under compulsory motor liability insurance at VSK.

The cost of compulsory motor liability insurance after an accident is discussed here.

Checking OSAGO on the RSA website

Every motorist is required to be insured under MTPL, but, unfortunately, not everyone conscientiously draws up contracts with an insurance company. In the event of an accident, the injured party can check the MTPL policy of the culprit using the PCA database to verify the authenticity of the insurance.

RSA has provided everyone with the opportunity to check their compulsory motor liability insurance online. We remind you that with us you can verify the authenticity of the policy using the PCA .

The following types of checks are available in 2021:

- By insurance number. You must log in to the RSA website, fill out the form provided, entering information about the document, go through a security check and confirm the request using the “Search” button. The system will provide information in the form of a table, which will indicate the date, status, name of the insurer, and period of validity of the policy.

- According to the VIN of the car. To obtain information, go to the RSA website, select the link corresponding to the request, enter the series and number indicated in the form in the fields that open, confirm security and click “Search”. The registration number, body number or VIN, document status and name of the insurer will appear on the screen.

- By license plate number. If an accident happens on the road, the victim can quickly check the vehicle's license plate number.

- By owner's last name. You can accurately find out about the authenticity of the purchased document by the owner’s last name at the office of the insurance company, since one last name is not enough to obtain all the information you need.