When and how should I pay?

For the first time, investors will pay this tax only in 2022. Banks will transmit the information to the Federal Tax Service, and the tax office will independently calculate the amount of tax and send a notification to the individual. Citizens will not need to declare such income or formalize them in any way.

I keep money in different accounts, for each separately the interest income will not exceed the limit. I won't pay tax?

You will, since the total income from all accounts is taken into account. That is, if the income on one account is 20 thousand rubles, and on the other – 30 thousand rubles, then in total it will exceed 42.5 thousand rubles, and you will have to pay tax on the “extra” 7.5 thousand rubles.

I opened a deposit back in 2021 for three years. Will I have to pay taxes on the interest?

Interest will be taken into account for the period in which it is actually received.

If interest is paid at the end of the deposit period (in our case this is 2021), then you will have to pay tax on ALL income.

If interest is calculated, for example, once a month, then tax will have to be paid ONLY on income for 2021 and only if it exceeds 42.5 thousand rubles.

In the current conditions, deposits with monthly, quarterly or annual interest payments are becoming the most profitable. In this case, you will protect income in the amount of 42.5 thousand rubles from taxes every year. That is, in a year you will save (at the current key rate) 5 thousand 525 rubles, in two years - 11 thousand 50 rubles, and in three years - 16 thousand 575 rubles.

If you enter into an agreement under which interest payments will occur in two, three or four years, then your savings over the entire period will amount to a minimum of 5 thousand 525 rubles.

If the deposit is closed early, will I have to pay tax?

If the amount of income exceeds 42.5 thousand rubles, then yes, you will have to pay.

How will taxes be collected from foreign currency deposits?

Interest paid to an individual on foreign currency accounts will be converted into rubles at the official exchange rate of the Bank of Russia on the day of actual receipt of this income.

The Central Bank has determined on what amounts the deposit tax will be levied in 2021

From January 1, 2021, the flat scale of taxes on personal income has been abolished in Russia (remember, it was 13% for everyone). Now citizens whose income is above 5 million rubles per year (on average - 416.7 thousand per month) , will pay more. The rates look like this:

13 percent - if the total income is equal to 5 million rubles or below this amount.

15 percent – if the total income is above 5 million rubles. Tax is imposed on:

- wage,

- dividends,

- winnings

- and other income

The full list can be found in the Tax Code (clause 2.1, article 210).

Irregular income is excluded from the calculation:

- income from the sale of property,

- present,

- insurance payments.

- Published in No. 025 dated 02/12/2021.

Currently, in order to receive a deduction for the costs of purchasing housing and repaying mortgage interest, you must submit a declaration in Form 3-NDFL and supporting documents to the tax office.

Naturally, this process is difficult and time-consuming.

It takes a long time to fill out a declaration, especially for those taxpayers who are far from following the rules for completing it. This forces many citizens to turn to specialists who prepare the necessary documents for a monetary reward of 500 rubles or more.

In addition, not everyone likes to visit the tax office and waste their time on bureaucratic procedures.

With the adoption of the law, the procedure for obtaining a tax deduction will be significantly simplified.

There is no need to fill out a declaration in Form 3-NDFL and submit supporting documents to the tax office. It will be enough to send an application for a tax deduction through the taxpayer’s personal account, and the tax office itself will collect the necessary information and transfer the amount of overpaid taxes in connection with the provision of the deduction to the account specified in the application.

At the same time, the simplified procedure does not deprive the taxpayer of the right to receive a deduction in the general manner. That is, everyone decides for themselves whether to use the simplified procedure or fill out a declaration and contact the tax office in person.

If receiving a tax deduction in the general procedure requires 4 months from the date of submission of the declaration and relevant documents, then under the simplified procedure this period is reduced by more than 2 times and amounts to 1.5 months, of which:

- period of desk audit - 1 month;

- the deadline for sending an order to transfer funds to the treasury is 10 days;

- The deadline for transferring money to the taxpayer is 5 days.

The bottom line: changes have also occurred in terms of income tax. Until 2021, the personal income tax rate was fixed - 13% for everyone. Since the new year, for citizens with high incomes, personal income tax has increased to 15.

For those whose annual income does not exceed 5 million rubles. nothing has changed - these citizens still pay 13% income tax. Such people are the majority in our country.

For those whose annual income exceeds 5 million rubles, from 2021 there will be an increased personal income tax rate of 15%, but with a caveat - only the excess amount will be subject to the increased rate (in other words, only that which is more than 5 million rubles). There are few citizens with such incomes in Russia - about 1-2% of the total population.

In this case, it will be income that will be considered income - the amounts regularly received by a person (from salary, dividends, etc.). If a citizen sold an apartment or other personal property for more than 5 million rubles, then he does not need to worry - no one will force him to pay 15% personal income tax.

The bottom line: you can now become self-employed in any region of Russia. Young people from 16 to 18 years old who registered as self-employed for the first time after January 1, 2021, will receive an additional tax bonus of 12.1 thousand rubles. This amount can only be spent on paying tax for self-employed people - other options, including withdrawing the bonus in cash, are not provided for by law.

The starting tax deduction of 10 thousand rubles, which every newly registered self-employed person receives, has also not gone away. Thus, young people who started working for the first time in 2021 will be able to receive a total of 22.1 thousand rubles. tax bonus, which will reduce the tax amount monthly.

Thus, in 2021, many Russians will have to pay more taxes, although relief is expected for a number of citizens.

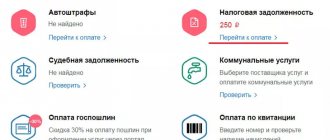

According to Article 409 of the Tax Code of the Russian Federation, the payer must pay the tax before December 1 of the year following the previous tax period. The tax office sends a notification to the citizen, on the basis of which payment is made.

Cadastral value is a more reliable indicator of the assessment of real estate of individuals, which is established as a result of an examination. The transfer of real estate tax taking into account the cadastral value will take place for the first time in 2021.

- The calculation of property tax for Russian citizens in 2021 will be based on the cadastral value of the property.

- Owners of real estate can receive a tax deduction, which is equal to the cadastral value of a certain number of square meters in relation to a specific type of property: 50 - if you own a house, 20 - if you own a property in the form of an apartment or part of a house, 10 - if you own part of an apartment or a room.

- Depending on the type of property, tax rates are different and amount to 0.1; 0.5; 2%. Payment must be made based on the notification sent by the tax office.

- Beneficiaries may be exempt from paying for one house or apartment, one garage or place for a car. If you own a second and third object, then payment of tax is required.

Foreign organizations and individuals will be able to indicate “0” in the “TIN of the payer” field if they are not registered with the tax office. An exception is payments administered by tax authorities. The amendment comes into force on January 1, 2021.

When deducting money from the income of an individual debtor to pay off the debt, indicate his TIN in the “TIN of the payer” field. It is no longer possible to enter an organization’s TIN from July 17, 2021.

If a payment order was drawn up by an individual without an account and intends to transfer money to the budget using it, the details must indicate the individual’s tax identification number or “0” if the number has not been assigned. It is prohibited to indicate the TIN of a credit institution. This rule is effective from October 1, 2021.

The main change concerns individual entrepreneurs, notaries, lawyers and heads of peasant farms. From October 1, 2021, payer status codes “09”, “10”, “11” and “12” will no longer be valid. Instead, the taxpayers listed above will indicate code “13,” which corresponds to individual taxpayers.

Also, some of the codes will be deleted or edited. New codes will be added:

- “29” - for politicians who transfer money to the budget from special election accounts and special referendum fund accounts (except for payments administered by the tax office);

- “30” - for foreign persons who are not registered with the Russian tax authorities, when paying payments administered by customs authorities.

Tax notice

The tax authority calculates tax based on the data it has on the property of individuals

:

- For transport tax (clause 3 of Article 363 of the Tax Code of the Russian Federation);

- For land tax (clause 4 of article 397 of the Tax Code of the Russian Federation);

- For property tax for individuals (Article 408 of the Tax Code of the Russian Federation).

In this case, the tax authority sends the taxpayer a tax notice, on the basis of which the tax is paid.

The tax notice must be sent by the tax authority to the taxpayer no later than 30 days before the payment deadline (Clause 2 of Article 52 of the Tax Code of the Russian Federation). Since the tax payment deadline is December 1st

, then the tax notice must be sent to the taxpayer

no later than November 1

.

If a tax notice is not received by November 1, the Federal Tax Service of Russia recommends one of three options:

- Contact the tax office. You can contact any tax office (with the exception of interregional tax inspectorates and inspectorates for centralized data processing).

- Submit information through the “Taxpayer Personal Account”.

- Contact the tax office using the Internet service “Contact the Federal Tax Service of Russia.”

If you have not resolved the issue of receiving a tax notice by the tax payment deadline, you can take advantage of the opportunity to pay the Unified Tax Payment of an individual in order to avoid paying penalties for late payment of tax. True, in this case you will not have the exact amount of tax debt. But you can use last year’s tax amounts as a basis.

The obligation of individuals to notify the tax authorities about their real estate and vehicles.

An obligation has been established for individuals to notify tax authorities about their real estate and vehicles. Such an obligation is established only if the individual has not received a tax notice with information about the purchased object.

New deadlines for payment of basic taxes and contributions in 2021: table

This field indicates the document number that is the basis for the payment. Its completion depends on how field 106 is filled in.

The new code for the basis of payment in the four invalid cases is “ZD”. But despite this, the deleted codes will appear as part of the document number - the first two characters. Fill out the field in the following order:

- “TR0000000000000”—number of the tax office’s request for payment of taxes, fees, and contributions;

- “AP0000000000000” - number of the decision to prosecute for committing a tax offense or to refuse to prosecute;

- “PR0000000000000” - number of the decision to suspend collection;

- “AR0000000000000” – number of the executive document.

For example, “TR0000000000237” - tax payment requirement No. 237.

The procedure for filling out field 109 changes to pay off debts for expired periods. When specifying the “ZD” code, you need to enter in the field the date of one of the documents that is the basis for the payment:

- tax requirements;

- decisions to prosecute for committing a tax offense or to refuse to prosecute;

- decisions to suspend collection;

- writ of execution and initiated enforcement proceedings.

The single tax on imputed income or UTII, relevant for LLCs/IPs, replaces the profit/income tax of individuals, property tax and value added tax. It can only be paid by bank transfer.

Enterprises or individual entrepreneurs that meet the following criteria can use UTII:

- Are not registered as payers of the single agricultural tax;

- Conduct work under a simple partnership agreement, trust management, joint activity;

- They have a staff of no more than one hundred people;

- Do not belong to the largest taxpayers;

- Occupy an area of less than 150 square meters. meters.

The problem with this type of taxation is that it is calculated based on physical indicators (number of employees employed in production, area of premises, number of vehicles, etc.), and not as a percentage of the real income of the company (IP).

This approach is not objective, which is why they want to abolish UTII. The final decision has not yet been made, but the Ministry of Finance claims that the tax will still be abolished. The exception is the Republic of Crimea, where the single tax on imputed income has been officially extended until 2024.

Despite the lack of confirmation of changes, the Federal Tax Service is already notifying payers about the abolition of UTII through newsletters, advertising banners, articles in the media and leaflets posted in tax offices.

Transport and land taxes are combined into one group, since they received the same changes:

- Cancellation of tax returns (starting from 2021);

- Adjustment of deadlines for making advance payments and paying taxes (full payment for the past year must occur no later than March of this year);

- Enterprises and the Federal Tax Service Inspectorate calculate the tax amount independently of each other, after which the Federal Tax Service Inspectorate sends the results of its calculations to the organization.

If the company believes that it should pay less, then it provides supporting documents to the tax office. As a result of their consideration, a final decision is made: either the amount of tax remains the same, or it is reduced in favor of the enterprise.

Taxes for individuals 2021

The main adjustment regarding personal income tax is an increase in the rate from 13% to 15%. However, the new coefficients will not apply to all taxpayers, but only to those whose annual income exceeds 5,000,000 rubles. All other citizens of the Russian Federation will continue to pay personal income tax according to the old rules.

So, for example, if an employee earned 5,100,000 rubles from January to June, then this money will be subject to 13% tax. As for the total salary from July to December, you will have to pay tax on it with an increasing coefficient.

In addition, changes were made to the taxation procedure for interest on deposits and bank account balances. If they exceed the non-taxable interest income, then they are charged a 13% rate. Another amendment concerns the unification of reporting: starting from 2021, 2-NDFL and 6-NDFL will be submitted jointly as part of 6-NDFL.

The last point worth mentioning is the personal income tax deduction for treatment. The list includes the following services:

- honey. evacuation;

- orthopedic therapy for people suffering from congenital or acquired dental defects;

- palliative care.

In addition, the list of expensive services related to reproductive technologies was replenished and expanded.

From 2021, it is planned to introduce a single tourist tax for foreigners wishing to visit St. Petersburg. The initiative, voiced by Governor Alexander Beglov, was approved by Vladimir Putin. In the new year, foreign guests of the Northern capital will have to pay 100 rubles for each day of stay.

Officials claim that the money collected in this way will be used to maintain cleanliness and order in St. Petersburg, reconstruct dilapidated historical buildings and develop the city's tourism infrastructure.

The so-called “resort fee” is a common phenomenon that makes it possible to maintain and regularly update tourist sites with high attendance. Guests from Germany, Spain, Italy, the Czech Republic, Montenegro, France, Greece, Lithuania and a number of other European countries pay an amount from 0.25 to 5 euros per night.

Starting from 2021, the list of income of individuals not subject to insurance premiums is expanding (Federal Law No. 374-FZ dated November 23, 2020). This list is supplemented by monetary compensation received by contractors and performers from customers to reimburse expenses associated with the performance of work and provision of services under civil contracts.

At the same time, amounts received by performers under civil contracts related to reimbursement of expenses for payment for residential premises are exempt from insurance premiums (future edition of clause 1 of Article 422 of the Tax Code of the Russian Federation).

From 10/01/2021, taxpayers will have to use the new electronic format of the adjustment invoice (Order of the Federal Tax Service of Russia dated 10/12/2020 No. ED-7-26/736). Until this time, it is allowed to use both the new electronic format and the approved format. by order of the Federal Tax Service of Russia dated April 13, 2016 No. ММВ-7-15/ The updated format of the adjustment invoice takes into account changes in legislation, including those related to the introduction of a system of mandatory traceability of goods.

From 01/01/2021, corporate income tax will be reduced for IT companies (Federal Law dated 07/31/2020 No. 265-FZ).

In accordance with the law, IT companies will be able to pay income tax only to the federal budget at a rate of 3%, subject to a number of strict conditions. In order to apply this benefit, the share of income from IT services must be at least 90% of the organization’s total income, and its staff must employ at least 7 people. Clarifications and clarifications on the application of Law No. 265-FZ are expected.

For publishing houses and the media (media), from January 1, 2021, the rules for writing off the cost of unsold printed products as expenses are changing (Federal Law No. 323-FZ of October 15, 2020).

Currently, publishing houses and the media are allowed to include no more than 10% of the cost of the unsold circulation of the corresponding issue of a periodical printed publication or the corresponding circulation of book products as other expenses for income tax purposes. Starting from the new year, this limit increases to 30%.

From January 2021, the list of information included in the tax return for property tax of organizations is expanding (Federal Law No. 374-FZ dated November 23, 2020). According to the new rules, the tax return will have to include information on the average annual value of not only real estate, but also movable property.

We are talking about movable property recorded on the organization’s balance sheet as fixed assets in the manner established for accounting. At the same time, movable property of organizations will still not be taxed.

For organizations, from 01/01/2021, the deadlines for payment of land tax and advance payments for this tax will change (clause 68 of Article 2 of Law No. 325-FZ).

Starting from the new year, land tax must be paid by organizations no later than March 1 of the year following the expired tax period. By analogy with transport tax, advance payments for land tax will also be paid no later than the last day of the month following the expired reporting period.

Personal income tax (NDFL)

The personal income tax return (3-NDFL) is submitted no later than April 30 of the year

, following the expired tax period (clause 1 of article 229 of the Tax Code of the Russian Federation (TC RF))[ 1 ].

Personal income tax is paid at the taxpayer’s place of residence no later than July 15 of the year following the expired tax period (clause 4 of Article 228 of the Tax Code of the Russian Federation).

In some cases, individuals who are not individual entrepreneurs must themselves submit a tax return for personal income tax (NDFL) and pay tax to the budget. This situation arises, for example, if an individual receives dividends from a foreign organization.

Personal income tax 2021: key changes for citizens and businesses

If, due to the lack of money in the debtor’s accounts for two months or due to the closure of the account, the bank was unable to fulfill the order of the tax authorities to forcibly write off the debt, the writ of execution is sent to the bailiffs to collect the debt at the expense of the citizen’s other property.

Companies and individual entrepreneurs with employees act as tax agents in relation to the income they pay to employees. In this regard, there is a need to pay insurance premiums and income taxes in 2021 for employees.

- the payer sold property (apartments, cars) that he owned for less than the minimum period of ownership;

- any property was donated to an individual by someone other than his close relatives;

- the payer received income from the rental of property or other income from those who were not tax agents in relation to such income;

- an individual won the lottery;

- the income was received from a foreign source.

The patent system, as established in Art. 346.43 of the Tax Code of the Russian Federation, can only be applied by individual entrepreneurs, and the payment period will directly depend on the duration of the period for which the patent is acquired. If it does not exceed 6 months, then the payer must transfer the full amount of tax to the budget on any day before the patent expires.

Tax on the sale of a car must be paid if you owned the car for less than three years, or the amount of its sale was more than what you bought it for, that is, you made a profit. Otherwise, you do not have to pay tax, but you still need to file a declaration on the sale of the car.

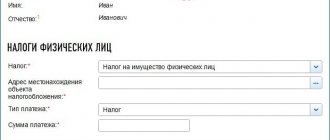

Property tax is paid annually by every citizen who owns any property. For this tax, the Federal Tax Service usually sends out payment slips on its own, which calculates the amount of tax and there are no problems with this. The tax is calculated based on the cadastral value of the object and ranges from 0.1 to 0.5% of the cadastral value of the object. You can receive tax deductions and various benefits and reduce the cost of the tax.

- go to the official website of the authorized body;

- enter your password and log into your personal account. It must be taken into account that only those persons who know the password can have access to the personal account, that is, the taxpayer should not worry that other persons can use the personal account without the knowledge of the car owner. You can obtain a password from the tax office;

- click on the tab with taxes for individuals;

- choose a vehicle that is subject to taxation;

- press the “pay taxes” button;

- generate a payment order;

- The tax should be paid using online payment systems, through a bank or Internet banking, which will require the taxpayer a few minutes. It should be noted that through the State Services portal, the car owner can only find out the amount of tax, but can make the payment in other ways, for example, by credit card online, etc.

- the payer sold property (apartments, cars) that he owned for less than the minimum period of ownership;

- any property was donated to an individual by someone other than his close relatives;

- the payer received income from the rental of property or other income from those who were not tax agents in relation to such income;

- an individual won the lottery;

- the income was received from a foreign source.

The patent system, as established in Art. 346.43 of the Tax Code of the Russian Federation, can only be applied by individual entrepreneurs, and the payment period will directly depend on the duration of the period for which the patent is acquired. If it does not exceed 6 months, then the payer must transfer the full amount of tax to the budget on any day before the patent expires.

- In a fixed amount (in the Federal Compulsory Compulsory Medical Insurance Fund and the Pension Fund of the Russian Federation) with an income amount of no more than 300 thousand rubles. Contributions must be made no later than December 31 of the current year.

- Additionally, in the amount of 1% of income, if income from the business (or imputed/potential income for individual entrepreneurs on UTII or PSN, respectively) exceeded 300 thousand rubles. This additional contribution must be made by the end of July 1 of the following year.

Payments for property taxes were issued to most individuals in Russia at the end of September 2021. Many people today use their personal account on the tax service website or receive a notification about the need to pay taxes in their personal account on the government services portal. For such advanced taxpayers, paying taxes will be an extremely simple task - you can pay them directly on the Internet using a bank card.

For those who prefer the old way of paying taxes, there are paper receipts. You need to go to any bank branch with receipts and pay taxes there. However, it is possible that the bank will take its own commission.

New taxes from January 1, 2021

In addition to housing, the real estate group includes taxes on garages, parking spaces, rooms, houses, unfinished construction projects, etc. If an individual does not have any special benefit, he is obliged to pay the calculated amount of real estate tax.

To prevent the blow to the budget of families who own land plots of any category from being too strong, legislators decided to increase the tax in several stages. This means that the cadastral value will increase gradually – by 20% annually. Thus, the land tax will gradually increase, and by 2021 it will reach the full amount.

In terms of property taxes, payers - companies need to take into account:

- updating the property tax return form;

- cancellation of declaration of transport and land taxes (we no longer report for 2020);

- a new obligation to inform tax authorities about the objects of taxation of TN and ZN if they have not sent a tax notice;

- changing the procedure for paying transport and land taxes and advances on them.

Important! From 2021, organizations pay TN and ZN for the year no later than March 1 of the next year, and advances no later than the last day of the month following the reporting quarter. The timing of advance payments is no longer set by regional authorities (clause 68 of Article 2 of Law No. 325-FZ of September 29, 2019). For example, the advance payment for the 1st quarter of 2021 must be paid no later than 04/30/2021.

There will be amendments to the Tax Code of the Russian Federation regarding the payment of tax on lost and destroyed vehicles.

Traditionally, the minimum wage has been increased. Its approved size is RUB 12,392. But there is a possibility that the procedure for calculating the minimum wage and, accordingly, its size will change.

The tax office will have fewer reasons not to accept the declaration, and they will be recorded directly in the Tax Code of the Russian Federation, and not in the regulations, as now.

Tax authorities will warn taxpayers about blocking accounts for failure to submit reports.

For transactions with some goods, you will have to submit a new report to the Federal Tax Service.

Some tax payment details will change. BCCs from 2021 will be determined by a new order of the Ministry of Finance (there will also be new BCCs for personal income tax). But the government decided not to change the payment rates for new tax assessments.

The SME register will be updated not once a year, but monthly. From 01/01/2021, the details and procedure for filling out travel forms will be updated.

And good news: December 31, 2021 will be a day off.

The deadline for paying the property tax of organizations and the deadline for paying advances on this tax are established by the laws of the constituent entities of the Russian Federation.

Deadline for payment of transport tax in 2021

From 2021, the deadlines for payment of transport tax and advance payments on it will change. If before 2021 payment deadlines were established by the laws of regional authorities, then from 2021 specific deadlines have been established in the Tax Code. So, transport tax/advance payment in 2021 is paid within the following terms:

| Period for which tax/advance is paid | Payment deadline |

| For 2021 | 01.03.2021 |

| For the first quarter of 2021 | 30.04.2021 |

| For the second quarter of 2021 | 02.08.2021 |

| For the third quarter of 2021 | 01.11.2021 |

| For 2021 | 01.03.2022 |

From 2021, the deadlines for paying land taxes will also change. Tax/advance payments must be paid no later than the following dates:

| Period for which tax/advance is paid | Payment deadline |

| For 2021 | 01.03.2021 |

| For the first quarter of 2021 | 30.04.2021 |

| For the second quarter of 2021 | 02.08.2021 |

| For the third quarter of 2021 | 01.11.2021 |

| For 2021 | 01.03.2022 |

Land tax

Land tax is payable by individual taxpayers no later than December 1 of the year

following the expired tax period (clause 1 of Article 397 of the Tax Code of the Russian Federation).

Taxpayers - individuals pay tax on the basis of a tax notice sent by the tax authority (clause 4 of Article 397 of the Tax Code of the Russian Federation).

Taxpayers are organizations and individuals who own land plots recognized as an object of taxation in accordance with Article 389 of this Code, on the right of ownership, the right of permanent (perpetual) use or the right of lifelong inheritable possession, unless otherwise established by this paragraph (clause 1 of Art. 388 Tax Code of the Russian Federation).

The object of taxation is land plots located within the municipality (federal cities of Moscow, St. Petersburg and Sevastopol), on the territory of which the tax was introduced (clause 1 of Article 389 of the Tax Code of the Russian Federation).

Property tax for individuals in 2021

"1.2.5. clothing made of genuine leather (coats, short coats, jackets, blazers, jackets, vests, jackets, raincoats, suits), carpets and carpet products, complex household electrical goods (except for household electric refrigerators and freezers, household washing machines).”

- From January 1, the payers (individual entrepreneurs and other persons not carrying out entrepreneurial activities*) additionally include individuals who are not registered as individual entrepreneurs, but carry out types of activities recognized as the object of taxation as a single tax for individual entrepreneurs.

In connection with the entry into force of the Tax Code of the Republic of Belarus on the territory of Minsk, from February 1, 2021, new single tax rates for individuals who do not carry out entrepreneurial activities came into force, with the exception of foreign citizens and stateless persons, temporarily staying and temporarily residing in the Republic of Belarus, when selling goods, providing services (performing work).

18. Caring for adults and children, washing and ironing bed linen and other things in citizens’ households, walking and caring for pets, purchasing groceries, washing dishes and cooking in citizens’ households, paying fees from the person being served for use residential premises and housing and communal services, mowing grass on lawns, cleaning green areas from leaves, grass clippings and garbage, burning garbage

Separate requirements are imposed on employers - they must pay income tax (personal income tax) monthly on income accrued in favor of staff. In relation to personal income tax, the repayment of obligations is subject to compliance with certain features (Article 226 of the Tax Code of the Russian Federation):

The table reflects the deadlines for paying taxes in 2021, taking into account the postponement of payment deadlines. If the deadline coincides with a weekend/holiday, it is transferred to the next working date. For example, the water tax must be transferred to the budget by the 20th at the end of the quarter, but in January, April, July and October 2021, these days fall on weekends, so the tax must be paid on the next working day.

Payers are confused by the Tax Code norm that was in force in 2021. According to part six of Art. 188 NK-2021, the calculation and payment of real estate tax at increased rates stops from the 1st day of the first month of the quarter following the quarter in which the decision of the regional (Minsk City) Council of Deputies or, on its instructions, the regional (Minsk City) Executive Committee on exclusion of unused (inefficiently used) capital structures (buildings, structures), their parts from the list of unused (ineffectively used) property.

A capital structure (building, structure) for payer organizations is an object classified in accordance with the law for the purpose of determining the standard service life of fixed assets as a building, structure or transmission device

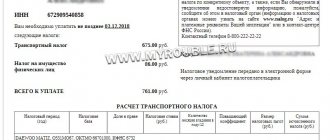

Transport tax

Transport tax is payable by individual taxpayers no later than December 1 of the year

following the expired tax period (clause 1 of Article 363 of the Tax Code of the Russian Federation).

Taxpayers - individuals pay transport tax on the basis of a tax notice sent by the tax authority (clause 3 of Article 363 of the Tax Code of the Russian Federation).

Taxpayers are persons who, in accordance with the legislation of the Russian Federation, have registered vehicles that are recognized as an object of taxation in accordance with Article 358 of this Code, unless otherwise provided by this article (Article 357 of the Tax Code of the Russian Federation).

The objects of taxation are cars, motorcycles, scooters, buses and other self-propelled machines and mechanisms on pneumatic and caterpillar tracks, airplanes, helicopters, motor ships, yachts, sailing ships, boats, snowmobiles, motor sleighs, motor boats, jet skis, non-self-propelled (towed vessels) and other water and air vehicles (hereinafter in this chapter - vehicles) registered in the prescribed manner in accordance with the legislation of the Russian Federation (Article 358 of the Tax Code of the Russian Federation).